In this month’s recap: Stocks stumbled as investors worried that the Fed would maintain its tight monetary posture due to ongoing inflation.

Monthly Economic Update

![]()

Presented by Ivana Lotoshynski, CFP®, March 2023

U.S. Markets

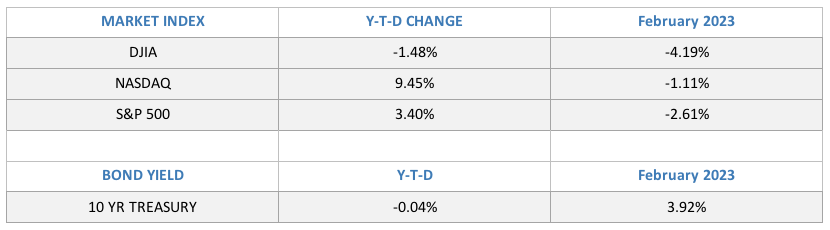

Stock prices stumbled in February owing to growing worries that the Fed would maintain its tight monetary posture in the face of continuing inflation.

For the month, the Dow Jones Industrial Average lost 4.19 percent, whereas the Standard & Poor’s 500 Index fell 2.61 percent. The Nasdaq Composite, up nearly 11 percent in January, dipped 1.11 percent.1

Strong Start Stumbled

The month began the way January ended-with stocks climbing higher on solid earnings reports and encouraging inflation data. The markets enthusiastically greeted the Fed’s 25-basis-point hike in interest rates, relieved that the increase was in line with expectations. Spirits were further lifted by constructive comments made by Fed Chair Jerome Powell following the rate hike announcement.

The optimism did not last long, however. Stocks struggled as the direction of future monetary policy weighed on investors throughout the month.

Uncertainty with Interest Rates

Despite an initial upbeat assessment by Powell at the post-meeting press conference, a strong employment report fanned fears that the Fed would be unable to pause rate hikes anytime soon.2

By mid-month, a higher-than-expected increase in consumer prices, strong retail sales numbers, and a rise in producer prices made it clear that the Fed would need to remain vigilant.

Stocks’ Slide Continued

The slide in stock prices continued into the end of the month, dragged down by further rate hike concerns and disappointing guidance from two major retailers that called into question consumer health. Stocks felt even more pressure after January’s Personal Consumption Expenditures (PCE) price index-the Fed’s preferred benchmark for gauging inflation-reflected hotter-than-expected price increases and vigorous consumer spending.2

Sector Scorecard

One silver lining regarding the difficult month was that the technology sector, one of the worst-performing groups in 2022, notched a slight gain of 0.41 percent.

The remaining sectors retreated, however, including industrials (_0.86 percent), communications services (_2.87 percent), consumer discretionary (_2.13 percent), consumer staples (_2.32 percent), energy (_6.94 percent), financials (_2.22 percent), health care (_4.64 percent), materials (_3.33 percent), real estate (_5.86 percent), and utilities (_5.92 percent).3

What Investors May Be Talking About in March

The Federal Open Market Committee (FOMC) is scheduled to meet on March 21-22, and the Fed at its previous meeting indicated that it intends to raise short-term interest rates by another 0.25 percent.4

However, the Fed will now need to digest fresh information on the labor market and inflation that may impact its upcoming rate decision.

Investors will be keenly parsing the FOMC meeting announcement accompanying the FOMC’s decision while also paying close attention to comments by Fed Chair Powell, who holds a press conference immediately following the meeting announcement.

In the Fed’s previous meeting, Powell acknowledged that a disinflationary trend has emerged, but he also cautioned that the Fed will evaluate the labor market and new inflation data for further guidance.

As such, it may be more Powell’s comments, rather than the expected rate hike, that move markets and set the tone for the weeks to follow.

![]()

T I P O F T H E M O N T H

Sometimes a sector or industry is touted as the “wave of the future” or the next hot trend. Beware of shifting your investment mix in response to hype or headlines – you may end up with a less diversified portfolio and greater exposure to risk.

![]()

World Markets

The prospect of higher rate hikes in Europe-and questions about the pace of China’s reopening-sent overseas stocks lower in February, with the MSCI-EAFE Index slipping 2.07 percent.5

European markets were higher, with Spain, Italy, and France leading the way. Germany picked up 1.57 percent, and the U.K. tacked on 1.35 percent.6

Pacific Rim markets trended lower, with China’s Hang Seng index dropping 9.41 percent and Australia’s ASX 200 falling 2.92 percent.7

Indicators

Gross Domestic Product: Gross Domestic Product: Economic growth in the fourth quarter was revised lower to 2.7 percent from its initial estimate of 2.9 percent. The downward revision was primarily attributable to lower consumer spending than originally estimated.8

Employment: New hires in January surged by 517,000, sending the unemployment rate to a 53-year low at 3.4 percent. Despite the robust job gains, wage growth remained below inflation, rising 4.4 percent from the previous January. The labor force participation rate slightly rose to 62.4 percent.9

Retail Sales: Consumer spending rebounded in January, climbing 3.0 percent. Retail sales exceeded estimates, coming off two consecutive months of declines.10

Industrial Production: Industrial production was unchanged in January, dragged down by a drop-off in utilities output owing to an unseasonably warm January. Manufacturing and mining increased production after two months of decline, rising 1.0 percent and 2.0 percent, respectively.11

Housing: Housing starts dropped by 4.5 percent, with single-family home starts declining 4.3 percent. Year-over-year housing starts tumbled 21.4 percent.12

Sales of existing homes lost 0.7 percent from a month ago, falling to the lowest level in more than 12 years. Year-over-year sales declined by 36.9 percent.13

New home sales rose 7.2 percent, the highest rate in nearly a year. The unexpected increase was the result of a surge in sales in the South, with all other regions experiencing declining sales.14

Consumer Price Index: Consumer prices firmed in January, rising 0.5 percent. The gain was an increase from the prior month and higher than consensus estimates. However, the year-over-year increase of 6.4 percent came in below the prior month’s 12-month rise of 6.5 percent-the seventh consecutive month of year-over-year declines. Core inflation (which excludes energy and food) was 0.4 percent, whereas the year-over-year increase was 6.4 percent, a tick lower than December’s 6.5 percent year-over-year read.15

Durable Goods Orders: Durable goods orders declined 4.5 percent largely owing to a comparison anomaly in which a historically large order for aircraft was booked in December, leading to a month-over-month drop. Excluding transportation, orders were up 0.7 percent.16

![]()

Q U O T E O F T H E M O N T H

“In the business world, unfortunately, the rear-view mirror is always clearer than the windshield.”

WARREN BUFFETT

![]()

The Fed

The minutes from the last meeting of the FOMC indicated that nearly all members favored the decision to raise rates by a quarter percentage point.

However, some Fed governors indicated they were inclined to vote for, or would have also voted for, a 0.50 percent hike to more quickly achieve the Fed’s target range for short-term interest rates.

The minutes also suggested that the Committee may hike rates by a quarter percentage point at its next meeting, which is scheduled for March 21-22.17

Sources: Yahoo Finance, February 28, 2023.

Sources: Yahoo Finance, February 28, 2023.

The market indexes discussed are unmanaged and generally considered representative of their respective markets. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results. U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid.

T H E M O N T H L Y R I D D L E

T H E M O N T H L Y R I D D L E

While most English words can be pluralized by adding the letter S on the end, there is one word that can be pluralized just by the addition of the letter C. What is it?

LAST MONTH’S RIDDLE: What can you fill with empty hands?

ANSWER: Gloves.

![]() Ivana Lotoshynski, CFP® may be reached at 973-227-3390 or ILotoshynski@peoplewealthmatters.com

Ivana Lotoshynski, CFP® may be reached at 973-227-3390 or ILotoshynski@peoplewealthmatters.com

https://peoplewealthmatters.com/

Know someone who could use information like this? Please feel free to send us their contact information via phone or email.

(Don’t worry – we’ll request their permission before adding them to our mailing list.)

![]()

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs, or expenses. Investors cannot invest directly in indices. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index(r) (VIX(r)) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx(r), and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalization in the FTSE Developed Europe Index. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. Established in January 1980, the All Ordinaries is the oldest index of shares in Australia. It is made up of the share prices for 500 of the largest companies listed on the Australian Securities Exchange. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. The FTSE TWSE Taiwan 50 Index is a capitalization-weighted index of stocks comprising 50 companies listed on the Taiwan Stock Exchange developed by Taiwan Stock Exchange in collaboration with FTSE. The MSCI World Index is a free-float weighted equity index that includes developed world markets and does not include emerging markets. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The U.S. Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability, and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting, or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

CITATIONS:

1. WSJ.com, February 28, 2023

2. FoxBusiness.com, February 24, 2023

3. SectorSPDR.com, February 28, 2023

4. CMEGroup.com, February 28, 2023

5. MSCI.com, February 28, 2023

6. MSCI.com, February 28, 2023

7. MSCI.com, February 28, 2023

8. WSJ.com, February 23, 2023

9. CNBC.com, February 3, 2023

10. WSJ.com, February 15, 2023

11. FederalReserve.gov, February 15, 2023

12. Reuters.com, February 16, 2023

13. CBC.com, February 21, 2023

14. Bloomberg.com, February 24, 2023

15. WSJ.com, February 14, 2023

16. Morningstar.com, February 27, 2023

17. WSJ.com, February 22, 2023