In this month’s recap: Stocks surge on receding inflation and recession worries, and better-than-expected second-quarter earnings.

Monthly Economic Update

![]()

Presented by Ivana Lotoshynski, CFP®, August 2022

U.S. Markets

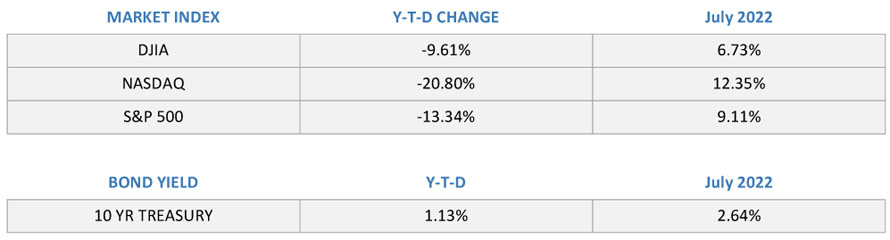

Stocks posted big numbers in July, erasing some of their first-half losses. Investor sentiment was lifted by receding inflation and recession worries and a better-than-expected start to the second quarter earnings season.

The Dow Jones Industrial Average gained 6.73 percent, while the Standard & Poor’s 500 Index rose 9.11 percent. The Nasdaq Composite led, picking up 12.35 percent.1

Hopeful Signs

Stocks have been under pressure all year from rising inflation and slowing economic growth. There weren’t many signs in July that suggested either inflation had cooled or that the economy was rebounding. Nevertheless, investors saw falling energy prices and persistent strength in the labor market as hopeful signs that any economic downturn may not be as severe as some expect.

Earnings Help Rally

Investor sentiment improved further as earnings season got underway in the back half of the month. This gathering optimism was not a result of exceptional earnings results. Rising enthusiasm was perhaps more attributable to the fact that earnings were not nearly as weak as many had feared. Companies painted a picture of a reasonably healthy consumer and businesses effectively navigating their inflation and supply chain challenges.

Big Week Of Data

The month of July culminated in perhaps the most critical week of the summer for the market, with investors awaiting information on corporate earnings, a Fed meeting decision on interest rates, and the release of an initial estimate of the second quarter GDP.

Investors Impressed

Earnings came out of the gate a bit shaky as a big box retailer missed earnings and guided future earnings estimates lower. However, subsequent earnings reports from big technology companies impressed investors. Markets were further relieved by the Fed’s decision to hike rates by 75 basis points and Fed Chair Powell’s comment that the pace of future rate hikes may slow.

Investors shrugged off a negative second quarter gross domestic product report as positive earnings surprises drove stocks higher into the close of the month.

Sector Scorecard

All 11 sectors posted gains for the month, including Communications Services (+3.87 percent), Consumer Discretionary (+18.44 percent), Consumer Staples (+3.20 percent), Financials (+7.19 percent), Health Care (+3.24 percent), Industrials (+9.50 percent), Materials (+6.15 percent), Real Estate (+8.52 percent), Energy (+9.66 percent), Technology (+13.45 percent), and Utilities (+5.45 percent).2

What Investors May Be Talking About in August

Historically, August has been positive for stocks, with an average return of 0.7 percent for the month. August also has more positive monthly performances (55) than negative (39).3

But August is also known for unexpected national and world events that have moved the markets in unexpected ways. Events that have occurred in August include the Asian currency crisis in 1997, the Long-Term Capital Management collapse in 1998, the downgrade of U.S. debt in 2011, and China’s currency crisis in 2015.

During the month, the government will release a string of economic reports to give the Fed fresh insight into the economy for its late September meeting. After September, the Fed only has two scheduled meetings for the rest of 2022-one in early November and one in mid-December.

![]()

T I P O F T H E M O N T H

As you retire, look at the changes in your expenses. Will your mortgage soon be paid off? What business-related expenses will disappear, and what new expenses will emerge? This may matter greatly in your retirement strategy.

![]()

World Markets

Overseas markets rallied following the lead of the U.S. markets. The MSCI-EAFE Index gained 3.74 percent last month.4

Similar to U.S. markets, major European markets overcame growing recession fears and deepening energy woes. France picked up 8.87 percent, Italy rose 5.71 percent, Germany 5.48 percent, and the U.K. tacked on 3.54 percent.5

Pacific Rim markets were mostly higher, except for Hong Kong, which lost 7.79 percent. Australia gained 5.74 percent and Japan climbed 5.34 percent.6

Indicators

Gross Domestic Product: The economy shrank at an annualized rate of 0.9 percent in the second quarter as consumer spending moderated and businesses reduced inventories. GDP posted its second straight quarter of negative growth, meeting the technical definition of a recession. Unlike most recessions, however, the past two quarters have been marked by strong employer hiring.7

Employment: Non-farm payrolls increased by 372,000 in June, with the unemployment rate unchanged at 3.6 percent. Wages increased 5.1 percent year-over-year.8

Retail Sales: Retail sales rose 1.0 percent in June, beating consensus estimates.9

Industrial Production: Industrial production declined 0.2 percent in June, though it was higher by 6.1 percent in the second quarter.10

Housing: Housing starts slipped 2.0 percent as rising prices and mortgage rates weighed on buyer demand. It was the second consecutive month of declines.11

Existing home sales fell 5.4 percent, while the median sales price climbed 13.4 percent to another record high of $416,000.12

New home sales declined 8.1 percent in June, falling to levels not seen since April 2020. Year-over-year sales were down 17.4 percent.13

Consumer Price Index: CPrices of consumer goods and services climbed 1.3 percent in June. The 12-month increase was 9.1 percent, a 40+ year high. Core inflation (excluding volatile food and energy prices) remained elevated as well, rising 0.7 percent from May’s levels and 5.9 percent from a year ago.14

Durable Goods Orders: Orders for products designed to last three years or more rose 1.9 percent. When excluding defense spending, durable goods orders were up a more modest 0.4 percent.15

![]()

Q U O T E O F T H E M O N T H

“The most valuable player is the one who makes the most players valuable.”

PEYTON MANNING

![]()

The Fed

Fed officials agreed to a 0.75 percentage point hike in the federal funds rate, acknowledging that the economy has slowed since the Federal Open Market Committee in June.16

In a post-meeting press conference Fed Chair Powell said that future rate hikes would be made on a meeting-by-meeting basis and that it may become appropriate to slow the pace of future interest rate hikes.16

Sources: Yahoo Finance, July 31, 2022.

Sources: Yahoo Finance, July 31, 2022.

The market indexes discussed are unmanaged and generally considered representative of their respective markets. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results. U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid.

T H E M O N T H L Y R I D D L E

T H E M O N T H L Y R I D D L E

Michael introduces Levi to his friends, stating that Levi’s father is also the son of Michael’s father. But Michael is an only child. So how are Michael and Levi related?

LAST MONTH’S RIDDLE: LAST MONTH’S RIDDLE: Tim says he heard that you can find $200 stuffed between pages 147 and 148 of a romance novel at the library. What detail convinces you that he is wrong?

ANSWER: The pagination. Page 147 is a right-hand page, page 148 would be the left-hand page printed on its reverse. So nothing could be kept between these pages.

![]() Ivana Lotoshynski, CFP® may be reached at 973-227-3390 or ILotoshynski@peoplewealthmatters.com

Ivana Lotoshynski, CFP® may be reached at 973-227-3390 or ILotoshynski@peoplewealthmatters.com

https://peoplewealthmatters.com/

Know someone who could use information like this? Please feel free to send us their contact information via phone or email.

(Don’t worry – we’ll request their permission before adding them to our mailing list.)

![]()

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs, or expenses. Investors cannot invest directly in indices. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index(r) (VIX(r)) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx(r), and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalization in the FTSE Developed Europe Index. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. Established in January 1980, the All Ordinaries is the oldest index of shares in Australia. It is made up of the share prices for 500 of the largest companies listed on the Australian Securities Exchange. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. The FTSE TWSE Taiwan 50 Index is a capitalization-weighted index of stocks comprising 50 companies listed on the Taiwan Stock Exchange developed by Taiwan Stock Exchange in collaboration with FTSE. The MSCI World Index is a free-float weighted equity index that includes developed world markets and does not include emerging markets. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The U.S. Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability, and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting, or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

CITATIONS:

1. WSJ.com, July 31, 2022

2. Sector.SPDR.com, July 31, 2022

3. Yardeni Research, Inc., 2022

4. MSCI.com, July 31, 2022

5. MSCI.com, July 31, 2022

6. MSCI.com, July 31, 2022

7. Bureau of Economic Analysis, July 28, 2022

8. Bureau of Labor Statistics, July 8, 2022

9. CNBC.com, July 15, 2022

10. FederalReserve.gov, July 15, 2022

11. WSJ.com, July 19, 2022

12. CNBC.com, July 20, 2022

13. MarketWatch.com, July 26, 2022

14. CNBC.com, July 13, 2022

15. WSJ.com, July 27, 2022

16. CNBC.com, July 27, 2022