How to Prepare for Tax Season

People Wealth Matters

Understand Where Your Federal Tax Dollars Go

In this guide, we will explore where your tax dollars go, some of the ways tax filing may look different, and what you can do to prepare. Keep in mind, this guide is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax, legal, and accounting professionals before modifying your strategy.

Before we dive into the upcoming tax brackets and what you can do to prepare for the upcoming tax season, it can be helpful to understand precisely how the government allocates your federal tax dollars.

In 2022, the federal government spent $6.27 trillion, which equals 25% of the nation’s gross domestic product. Further examination reveals that three significant areas of spending made up the majority of the budget.1

Medicare

Medicare accounted for $755 billion, or 12% of the budget, in 2022.1

Defense Spending

Another $767 billion, or 12% of the budget, was paid for defense and security-related international activities. The bulk of the spending in this category reflects the underlying costs of the Defense Department. This includes the cost of multiple defense initiatives and related activities, described as Overseas Contingency Operations in the budget.1

Social Security

Nineteen percent of the budget, or $1.22 trillion, was paid for Social Security, which provided monthly retirement benefits averaging $1,632 to over 48 million retired workers. Social Security also provided benefits to 3 million spouses and children of retired workers, 6 million surviving children and spouses of deceased workers, and 9 million disabled workers and their eligible dependents.1,2

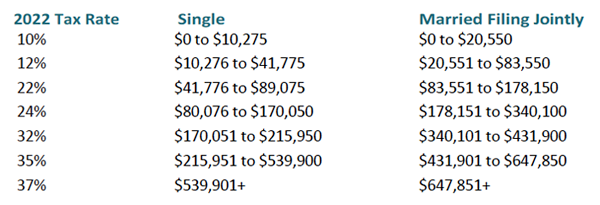

The Tax Brackets

The tax brackets are: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Here are the tax brackets and the corresponding income ranges.3

These modest changes to the tax brackets also mean that wage earners may fall into lower brackets. Here is one example. A single filer at $88,000 in taxable income would fall into the 24% bracket for tax year 2021. The filer would be in the 22% tax bracket in 2022. These new rates are scheduled to expire in 2025 unless Congress acts to make them permanent. Exemptions also changed under the new tax code.

Keep in mind that the tax brackets are representative of how much you will pay for each portion of your income. For example, if you make $100,000 for the 2022 tax year and are married filing jointly, you would pay 10% on the first $20,550, 12% on the next $63,000, and 22% on the final $16,450. You would not pay 22% for the entire $100,000 of your annual income.

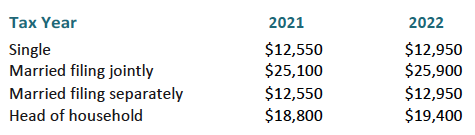

Here is an overview of the standard deductions over the past two years:3

IMPORTANT DEADLINES*

JANUARY 17, 2023

If you are self-employed or have other fourth-quarter income that requires you to pay quarterly estimated taxes, postmark this payment by January 17, 2023.

APRIL 18, 2023

FIRST QUARTER 2023 ESTIMATED TAX PAYMENT DUE

2022 INDIVIDUAL TAX RETURNS DUE

Most taxpayers have until April 18 to file tax returns. Email or postmark your returns by midnight on this date.

LAST DAY TO MAKE A 2022 IRA CONTRIBUTION

If you have not already contributed fully to your retirement account for 2022, April 18 is your last chance to fund a traditional IRA or a Roth IRA.

INDIVIDUAL TAX RETURN EXTENSION FORM DUE

If you cannot file your taxes on time, file your request for an extension by April 18 to push your deadline back to October 16, 2023.

JUNE 15, 2023

SECOND QUARTER 2023 ESTIMATED TAX PAYMENT DUE

SEPTEMBER 15, 2023

THIRD QUARTER 2023 ESTIMATED TAX PAYMENT DUE

OCTOBER 16, 2023

EXTENDED INDIVIDUAL TAX RETURNS DUE

If you received an extension, you have until October 16 to file your 2022 tax return.

*The IRS has the authority to adjust federal tax deadlines on short notice based on its assessment of financial or economic conditions. Also, please note that tax deadlines that fall on weekends or national holidays will be delayed until the following business day.

The Child Tax Credit

In 2021, the American Rescue Plan Act increased the child tax credit to up to $3,600 per child. Legislation to extend the 2021 child tax credit was not passed, so the credit reverted back to the 2020 credit of up to $2,000 per child for 2022. While the 2021 child tax credit was fully refundable, the 2022 tax credit is only partially refundable.

The 2022 credits phase out at income thresholds of $200,000 (or $400,000 for married taxpayers filing jointly).4

Preparing for the Tax Season

Planning well in advance of the tax season may help better prepare you for the unexpected. Here are several reasons to begin early:

- Your home, job, or relationships changed

- You need to start saving money if you may owe taxes

- You want to ensure you qualify for tax deductions

You can make changes throughout the year to ensure that your tax preparations go smoothly.

In particular, you can make periodic assessments of your paycheck witholdings so that you will get a refund or can reduce or eliminate your tax burden.

You should keep track of and store your tax and other financial records to avoid delays or frantic preparations as the filing deadline approaches. Records may include W-2 forms, canceled checks, certain receipts, and previous years’ returns.

Here is a list of other items to start gathering:

- Pay stubs

- Mortgage payment records

- Closing paperwork on home purchases

- Receipts for items or services you may want to claim as itemized deductions

- Records on charity giving and donations

- Mileage logs on cars used for business

- Business travel receipts

- Credit card and bank statements to verify deductions

- Medical bills

- 1099-G forms for state and local taxes

- 1099 forms for dividends or other income

During the first few months of 2023, make sure you receive your W-2 and 1099 forms as well as other tax documents. Leave adequate time to collect documents and prepare to file your taxes prior to the April 18, 2023 deadline.

Tightening the Nuts and Bolts

Here are some ways to prepare this year for next year’s tax season:

Look at last year: Take one more look at last year’s return. In the months ahead, you may still have the opportunity to contribute more to your retirement plan, which may lower your taxable income.

Donate to charity: How about “bunching” your charitable donations?

Bunching provides you with the ability to optimize your deduction allowances by making two or more years’ worth of charity donations in one year.

Let us say you are married, you expect to itemize your deductions, and you anticipate making $15,000 in annual donations. By donating $30,000 in one year and skipping the next, you may be able to qualify for a higher deduction.5

Review Capital Losses: If you are investing in the financial markets, you may want to consider deducting capital losses; you have the opportunity to claim deductions if you experienced losses.

You can claim losses only if they exceed capital gains. You are allowed to claim the difference of up to $3,000 per year if you are married filing jointly or $1,500 if you are filing separate returns. Net losses that exceed $3,000 can be carried over into future years.6

Deductions for capital losses can only be applied to investment property sales but not to the sale of investment property that was held for personal use.

Get organized: Find a place to store your tax documents until it is time to prepare to file. A good record-keeping system may alleviate concerns later as the deadline gets closer.

If you have your documents or prior-year returns stored on your computer, make sure you back them up on a thumb drive or other device or system in case your computer is hacked or stolen.

Consider other taxes: Keep an eye on local and state government requirements that may affect your specific tax situation.

How Long?

The IRS provides recommended timelines for retaining financial documents:7

- You should keep your tax records for three years if #4 and #5 below do not apply to you.

- You should keep records for three years from the original filing date of your return or two years from the date you paid your taxes. Select whichever is the later date. This is if you claimed a credit or refund after you filed your return.

- You should keep your records for seven years if you claimed a loss from worthless securities or a bad debt deduction.

- You should keep your records for six years if you failed to report income that you should have, and the income was more than 25% of the gross income listed on your return.

- Keep records indefinitely if you do not file a return.

- You should keep employment tax records for at least four years after the due date on the taxes or after you paid the taxes. Select whichever is later.

This Special Report is not intended as a guide for the preparation of tax returns. The information contained herein is general in nature and is not intended to be, and should not be construed as, legal, accounting or tax advice or opinion. No information herein was intended or written to be used by readers for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions. Readers are cautioned that this material may not be applicable to, or suitable for, their specific circumstances or needs, and may require consideration of non-tax and other tax factors if any action is to be contemplated. Readers are encouraged to consult with professional advisors for advice concerning specific matters before making any decision. This material was prepared by FMG, and the information given has been derived from sources believed to be accurate. This is not intended as a guide for the preparation of tax returns, nor should it be construed as legal, accounting or tax advice. This information is subject to legislative changes and is offered “as is”, without warranty of any kind. Publisher and provider assume no obligation to inform readers of any changes in tax laws or other factors that could affect the information contained herein.

Securities and advisory services offered through NEXT Financial Group, Inc., Member FINRA/SIPC. People Wealth Matters is not an affiliate of NEXT Financial Group, Inc.

Citations.

1. Treasury.gov, 2023

2. SSA.gov, 2023

3. IRS.gov, 2022

4. Investopedia.com, February 24, 2022

5. IRS.gov, 2022

6. IRS.gov, 2023

7. IRS.gov, 2022